What a supply chain 'Forged in Disruption' will mean for trucking

Key takeaways

- Truckload recovery is supply-driven as carrier exits tighten capacity, not a demand boom.

- AI adoption and automation are becoming essential tools for trucking productivity gains.

- Regulation, fuel costs, and global trade shifts are creating permanent freight market volatility.

The bumpy road for truckers isn’t going to get much better anytime soon; that’s the takeaway for for-hire truckload fleets from “Forged in Disruption,” the 2026 State of Logistics Report.

The message to the U.S. trucking industry: The era of predictable cyclicality is over. For fleet owners, 2026 is potholes and problematic—but offers opportunities for the nimble: geopolitical waffling, rapid AI integration, and daily-shifting trade rules. It's a “fog” of uncertainty that the industry must learn to drive through. So what else is new?

The Council of Supply Chain Management Professionals released the annual findings during a press briefing at the Empire State Building June 16. The publication is authored by global consulting firm Kearney and presented by Penske Logistics.

“The U.S. truckload market is exiting one of its longest downturns via a supply-driven reset, not a demand-led rebound. Regulatory pressures and fuel cost increases are accelerating carrier exits, tightening capacity sufficiently to firm pricing even as aggregate freight demand remains mixed,” the report opens. “The market now behaves less like a single national market and more like a collection of lane-level markets, with pricing, capacity, and service reliability varying sharply by corridor.”

As a result, major shippers are moving from annual bid cycles to “continuous, dynamic procurement” and a more strategic network architecture. Meanwhile, 2026 will not reward broad market assumptions.

“Carriers should avoid mistaking a supply reset for a demand boom,” the report suggests. “Shippers should avoid assuming that soft national freight indicators guarantee easy capacity.”

Broadly, U.S. business logistics costs (USBLC) came in at $2.4 trillion (7.8% of GDP) last year—a decline from 8.7% in 2024. The data suggests a deceptive normalization: While total expenditures have dipped due to softening ocean rates and flat rail revenues, complexity has reached an all-time high.

A panel of experts on hand for the report’s release, representing various freight modes and interests, cautioned that the current environment points to a fundamental shift from “buying power” toward decision-layer agility and resilience.

“When you’re in an industry where you can potentially put trucking companies out of business with network bids, you’ve got to be very, very cognizant of what you’re doing,” said Doug Cantriel, head of North American transportation and modernization at Ford. “When the last bids went through, it was very much a shipper’s market. That is shifting back. This is about the relationship, and this is where you work together when there are ebbs and flows.

“It's very critical that you build those relationships and don’t look at it as a hostile environment.”

Truckload market shifts to supply-driven recovery and tighter capacity

In outlining the report, lead author and Kearney partner Korhan Acar presented some basics from the trucking industry:

- Motor expenditures grew 1.7% in 2025, as carrier exits tightened capacity and supported a supply-driven recovery despite mixed freight demand.

- An end-of-2025 rate rally pushed spot rates higher as the truckload market entered a supply-driven recovery.

- Fuel inflation disproportionately impacted owner-operators and smaller fleets, contributing to supply-side exits.

- Montgomery v. Caribe Transport heightened focus on carrier vetting and risk management.

- Autonomous trucking is becoming commercially viable and could provide a long-term response to structural driver shortages, with near-term catalysts including the Autonomous Vehicle Acceleration Act (AVAA) and growing insurer willingness to underwrite autonomous fleets.

For fleets, the most critical takeaway from the 2026 report is that the market recovery is being driven by supply-side exits rather than a demand-led boom. Since 2022, an estimated 89,000 carriers have exited the market, finally thinning capacity enough to firm up pricing after a punishingly long downturn.

Andres Mendoza-Pena, a partner at Kearney and another report author, noted that the market has finally “turned the corner,” though he described it as a “long corner.” By early 2026, spot rates turned upward, compressing the gap and shifting leverage toward carriers. However, this reset is fragile. Unlike previous up-cycles, where demand surged, the current recovery is tied to capacity losses from smaller fleets and owner-operators.

Regulatory pressures, likewise, are becoming a structural constraint on capacity. Enforcement of English language proficiency (ELP) and non-domiciled CDL restrictions is creating localized tightness in specific corridors.

The Supreme Court’s May 2026 decision in Montgomery v. Caribe Transport has heightened broker liability. Brokers now must figure out how to document deeper scrutiny of carrier safety records, with some large brokers estimated to reduce their utilized carrier base by 20% to 30%, favoring fleets with auditable, high-standard safety profiles.

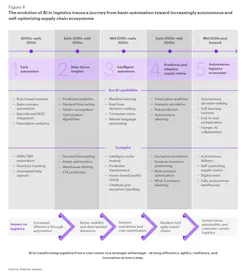

AI in trucking moves from hype to core freight operations tool

A new addition to this year’s report is the “State of AI in Logistics,” which argues that Artificial Intelligence has crossed the threshold from promise to proof. For motor carriers, AI is no longer a futuristic concept but a commercial necessity for managing a “transaction-heavy” industry.

Acar emphasized that AI value is now concentrated among early adopters who use it to automate repetitive work like quoting, scheduling, and exception management. Large brokers and carriers are reporting 30% increases in productivity by using generative AI to handle thousands of emailed quotes and load tenders daily.

The report outlines a framework of four AI capabilities: interpret, predict, recommend, and execute.

- Physical AI: 2026 marks a commercial milestone for autonomous trucking. Driverless services on corridors like Dallas-to-Houston are now operational, offering a long-term response to the driver shortage.

- Predictive maintenance: Platforms like FedEx’s MOBIUS are using AI to anticipate equipment failures, saving millions in potential downtime.

However, the “driver shortage” is a lingering challenge. Ford’s Cantriel suggested that the industry needs to focus on the “driver experience” and lifestyle rather than just numbers. He proposed the concept of “metro pilots”—leveraging local knowledge for final-mile delivery while autonomous systems handle the long-haul middle mile—allowing drivers to be home every night.

Global trade shifts and China+1 strategy reshape trucking freight lanes

Global trade policy has become a continuous operating variable, with U.S. tariffs changing on average every 1.5 weeks in 2025. This volatility has turned the “China+1” strategy into a permanent feature of corporate network planning. For ground carriers, this means a massive shift in the “center of gravity” for freight.

Beth Rooney, port director at the Port Authority of New York and New Jersey, stated that these changes are structural and permanent. Shippers are diversifying away from a China-centric model and moving toward Southeast Asia and Mexico. This has funneled massive volumes toward the southern border, making Mexico the largest U.S. trading partner for goods and turning border corridors into the fastest-growing lanes in the country.

Geopolitical instability in the Strait of Hormuz and the Red Sea has driven energy price volatility, with oil prices rising nearly 50% since late 2025. Paul Bingham, director of transportation consulting at S&P Global, noted that this creates a permanent risk premium, as energy shocks manifest rapidly through fuel surcharges and political risk insurance.

UP–NS merger could reshape rail competition and truckload diversion

The ground freight landscape is also being reshaped by the proposed Union Pacific–Norfolk Southern merger, which would create the first coast-to-coast single-line railroad in U.S. history. While the regulatory process continues through 2026, the strategic intent is to capture truckload diversion by improving transit times and eliminating interchange dwell in hubs such as Chicago.

If successful, the merger could move approximately 2.1 million trucks off the highway and onto rail. However, shippers remain divided, balancing potential service improvements against concerns about reduced competition and higher rates in captive markets. For motor carriers, this represents a new competitive front on high-density, long-haul lanes.

Fleet strategies for resilience in volatile freight markets

The expert panel urged fleet owners to design for resilience as a baseline condition, not an exception. Stacy Schlachter, senior VP of sales at Penske Logistics, noted that shippers are no longer paralyzed by disruption; they are actively adapting and expecting their partners to provide “decision intelligence.”

Key strategies for motor carriers in this “new normal” include:

- Prioritize asset productivity: In a high-cost-of-capital environment, efficiency gains from existing assets are more vital than aggressive expansion.

- Embed intelligence: End-to-end visibility and geopolitical intelligence are now core competitive capabilities, not back-office functions.

- Address “network drift”: Fleets must avoid the accumulated risk of reactive, incoherent adjustments by using scenario playbooks and AI to trigger real-time responses.

- Invest in leadership: As Cantriel noted, the profile of a logistician has shifted from a manager to a leader who can problem-solve across data, machines, and humans.

Driving through the fog

The defining challenge of 2026 is building the capabilities to perform consistently in an environment of permanent volatility.

As the industry moves from "navigating the fog" to operating within it, the competitive advantage will go to those who can sense, decide, and act in real time. Acar, the report’s lead author, concluded the presentation by suggesting that next year’s report be titled "Thriving in Disruption"—a testament to the resilience and adaptability required of the modern American motor carrier.

About the Author

Kevin Jones

Editor

Kevin has served as editor-in-chief of Trailer/Body Builders magazine since 2017—just the third editor in the magazine’s 60 years. He is also editorial director for Endeavor Business Media’s Commercial Vehicle group, which includes FleetOwner, Bulk Transporter, Refrigerated Transporter, American Trucker, and Fleet Maintenance magazines and websites.

Working from Beaufort, S.C., Kevin has covered trucking and manufacturing for nearly 20 years. His writing and commentary about the trucking industry and, previously, business and government, has been recognized with numerous state, regional, and national journalism awards.